Travel Insurance in 2026: What's Actually Covered, What Gets Denied, and How to Fight Back

You're two weeks from a $7,000 honeymoon to Italy. Your partner just got diagnosed with potential lymphoma. You call your travel insurance provider, certain you're covered. They tell you it's a pre-existing condition. Claim denied. That's not a hypothetical. Stories like this surface on travel forums constantly, and the details always catch people off guard. Travel insurance is supposed to be the safety net, but in 2026, the gap between what travelers think it covers and what it actually covers has never been wider.

Travel insurance typically covers trip cancellation for specific named reasons, emergency medical costs, evacuation, and baggage delays.

It does NOT cover pre-existing conditions (unless you buy a waiver within 14-21 days of your first deposit), war or military action, "change of mind" cancellations, or adventure sports without a rider.

Cancel For Any Reason (CFAR) policies cost 40-50% more but reimburse 50-75% of trip costs for any cancellation. If your claim gets denied, you can appeal with new documentation and escalate to your state insurance commissioner. One in three claims gets denied, and documentation problems are the top reason.

What Travel Insurance Actually Covers (and What It Doesn't)

A standard travel insurance policy covers four core areas: trip cancellation and interruption, emergency medical expenses, medical evacuation, and baggage loss or delay. That's the short version. The long version is where most people get surprised.

Trip cancellation reimburses your prepaid, non-refundable costs when you cancel for a "covered reason." Those reasons are explicitly listed in your policy, and they're narrower than you'd expect. Illness, injury, or death of the traveler or an immediate family member. Jury duty. A natural disaster at your destination. Terrorism at the destination. Mandatory evacuation orders. That's roughly the list for most standard policies.

What's NOT on that list: changing your mind, work conflicts, a breakup, fear of traveling, pandemic anxiety, or a destination you've simply lost interest in that doesn't directly prevent you from reaching your destination. Travelers routinely report that insurers reclassify legitimate illness cancellations as "change of mind," even when multiple doctors confirm the condition. Flu-related cancellations are a common flashpoint because insurers argue you could still physically travel.

Emergency medical coverage pays for hospital stays, doctor visits, prescriptions, and imaging while you're abroad. This matters because most domestic health insurance plans don't cover international care. The CDC's Yellow Book puts it plainly: if you need medical care in another country, you'll likely pay out-of-pocket, even in countries with nationalized health care.

Medical evacuation is where the numbers get scary. An air ambulance from a remote destination can cost $25,000 to over $250,000, depending on location. A helicopter medevac in Nepal? $150,000+. A Reddit user shared their experience being evacuated from Peru: the helicopter bill was $28,000, and their insurance covered every dollar. Without it, that's a second mortgage.

Baggage coverage reimburses you for lost or delayed luggage, usually up to a per-item and per-policy limit. Travel delay coverage kicks in when a covered delay lasts longer than 6-12 hours (depending on your policy), which reimburses meals, hotel stays, and transportation. If your flight gets cancelled, the DOT's automatic refund rule now requires airlines to refund you within 7 business days for credit card payments, but insurance fills the gap for non-refundable hotels and activities you'll miss.

The Pre-Existing Condition Trap in Travel Insurance

Pre-existing conditions are the single biggest source of travel insurance confusion, and the most common reason for denied claims that leave people genuinely angry. Here's how it works: every policy has a "look-back period," typically 60 to 180 days before your purchase date. If you had a medical condition that changed, was treated, or showed new symptoms during that window, it's classified as pre-existing and excluded from coverage.

"Stable" is the key word. If your doctor prescribed a new medication, adjusted a dosage, or ordered new tests during the look-back period, your condition isn't considered stable. That diagnosis of potential lymphoma two weeks before the Italy honeymoon? Pre-existing, because the diagnosis itself happened within the look-back window.

Most insurers offer a pre-existing condition waiver, but you have to buy your policy within 14-21 days of your first trip deposit, insure 100% of your non-refundable costs, and be medically able to travel at the time of purchase. Miss that window, and the waiver disappears. InsureMyTrip calls this the most commonly missed deadline in travel insurance.

The look-back period varies by insurer. Squaremouth's comparison data shows some plans use a 60-day window while others stretch to 180 days. A 60-day look-back is more forgiving: if your condition was stable for two months before you bought the policy, you're covered. A 180-day look-back means six months of stability, which eliminates coverage for anyone whose health has changed in the past half-year.

The practical takeaway: if you have any ongoing medical condition, buy your travel insurance the same week you make your first trip payment. Don't wait for the "right time." The right time is now. And read the look-back period before you buy, not after you file a claim.

War Zones, Airspace Closures, and the Middle East Crisis

In late February 2026, the US and Israel launched coordinated military strikes on Iran. The strikes triggered retaliatory missile and drone attacks across the region. CNBC reported that airlines cancelled hundreds of flights immediately, and within days, more than a million passengers worldwide were stranded as over 20,000 flights were grounded. (As of late March 2026, the insurance implications of this conflict are still developing.)

For anyone with a trip booked to the Middle East, the insurance question became urgent. The answer was brutal: standard travel insurance policies exclude war, acts of war (declared or undeclared), military operations, and government-ordered airspace closures. Allianz issued a coverage alert listing 15 "Impacted Countries" including the UAE, Qatar, Saudi Arabia, Egypt, Jordan, Bahrain, Kuwait, and Oman. Any policy purchased after March 1, 2026 wouldn't cover war-related disruptions to those destinations at all.

This caught travelers off guard because many of those countries weren't directly involved in combat. If you'd booked a Dubai layover on Emirates or a Doha connection on Qatar Airways, your insurance likely wouldn't reimburse the cancellation. The Insurance Journal reported that travelers stranded by the conflict were discovering their policies wouldn't cover flight cancellations caused by military action.

Standard travel insurance policies exclude coverage for military action, acts of war, political unrest, and government-related airspace closures. Many travelers affected by attacks in the Middle East may not qualify for financial reimbursement.

CNBC, March 2026

There's a narrow exception. If you already had a policy in force before the conflict began AND were already traveling or in transit to an impacted country on February 28, 2026, some insurers provided limited accommodation. Allianz, for example, covered additional accommodation and transportation expenses for those specific travelers, and waived their usual five-day maximum. But that's a small group.

The lesson here connects directly to how war is reshaping travel costs in 2026. If you're traveling to or through a region with active geopolitical tensions, a standard policy won't protect you. You need Cancel For Any Reason coverage, and you need to buy it before the situation escalates, because once a conflict is a "known event," insurers exclude it retroactively.

Cancel For Any Reason (CFAR): The Upgrade Worth Understanding

CFAR is the one policy type that covers what standard insurance won't: cancelling your trip because you simply don't want to go anymore. War broke out near your destination? Covered. Your gut says don't fly? Covered. Work emergency, family crisis, or just changed your mind? All covered. No documentation needed beyond cancelling at least 48 hours before departure.

Cost and reimbursement are the tradeoffs. CFAR typically adds 40-50% to your base premium, and some providers charge even more. Squaremouth's data confirms the 40-50% premium increase as typical, though some providers charge significantly more during peak demand periods. And you won't get a full refund: CFAR reimburses 50-75% of your non-refundable trip costs, not 100%.

Let's run the math on a real scenario. A $10,000 trip for two with a standard policy might cost $600-$700 in insurance (roughly 6-7% of trip cost). Adding CFAR bumps that to $900-$1,400. If you cancel, you'd get back $5,000-$7,500 of your $10,000. Without any insurance, you'd get $0.

| Coverage Type | Cost (on $10K trip) | Cancellation Payout | Covers War/Fear |

|---|---|---|---|

| No insurance | $0 | $0 | No |

| Standard policy | $600-$700 / ~€550-€650 | Up to $10,000 (named reasons only) | No |

| CFAR policy | $900-$1,400 / ~€830-€1,300 | $5,000-$7,500 (any reason) | Yes |

CFAR has strict purchase requirements. You must buy it within 14-21 days of your first trip payment, insure 100% of your prepaid non-refundable costs, and cancel at least 48 hours before departure. Miss any of these, and the CFAR benefit doesn't apply.

Is CFAR worth it? For a $2,000 weekend trip, probably not. For a $7,000+ international trip with non-refundable bookings during geopolitically unstable times? The math tilts heavily in favor of paying the extra premium. If you're planning a trip that involves your first international destination, the peace of mind alone changes how you experience the trip.

Adventure Sports and Travel Insurance: The Fine Print

You're snorkeling in Koh Tao when a sea urchin spine punctures your foot. The clinic visit costs $400. You file a claim. Denied. Snorkeling was listed under "hazardous activities" in a clause you never read.

Here's something most people discover too late: standard travel insurance excludes injuries from activities you'd consider normal vacation fun. Snorkeling. Riding a moped in Bali. Hiking above a certain altitude. Skiing, if your policy classifies it as "winter sports." Squaremouth notes that even common activities like biking, hiking, and scuba diving are frequently excluded from base policies because insurers classify them as high-risk.

If you're planning anything more adventurous than walking around a city, check your policy's exclusion list before you leave. Look for a section called "Sports and Activities" or "Hazardous Activities" in the certificate of insurance. The list is usually specific: bungee jumping, skydiving, hang gliding, heli-skiing, parasailing, caving, cliff diving.

U.S. News reports that adventure sports riders are widely available as add-ons in 2026. These riders cover search and rescue, security evacuation, and medical costs from covered activities. They add $20-$100 to your premium depending on the activity level. That's a small price compared to a $50,000 helicopter rescue in the Alps that your standard policy won't touch.

Moped and scooter injuries are one of the most common uncovered travel insurance claims, particularly in Southeast Asia. If your policy lists "motorized vehicles" or "motorcycles" under exclusions, that moped rental in Thailand isn't covered. Get the rider.

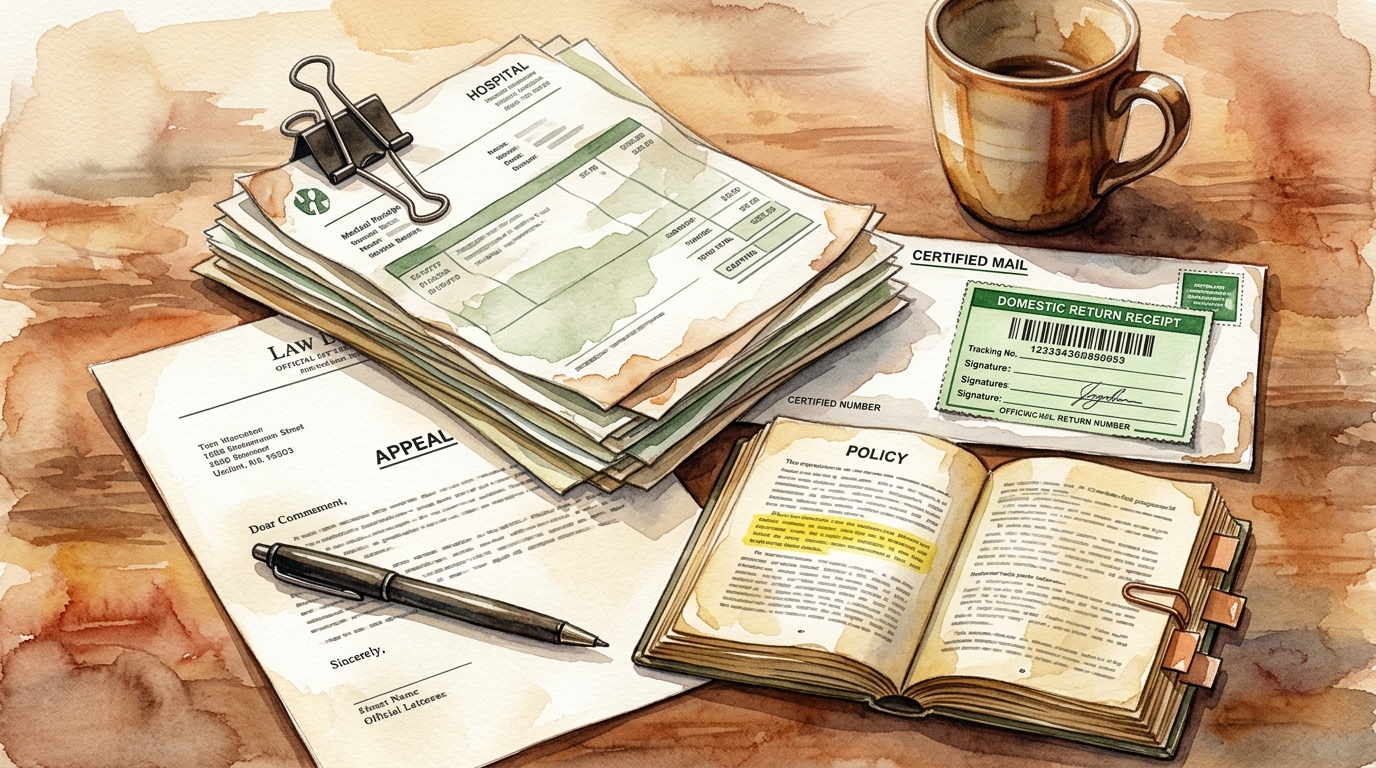

How to Fight a Denied Claim (and Win)

One in three claims gets denied, but that doesn't mean the insurer's decision is final. Squaremouth's claims data shows that documentation problems cause the largest share of denials. That means many denied claims are fixable.

- Read the denial letter carefully Understand exactly which policy clause the insurer is citing. If the language is unclear, call customer service and ask them to explain the specific exclusion or condition that triggered the denial.

- Gather NEW documentation Don't resubmit the same paperwork. Get a detailed letter from your doctor (specifying dates, diagnosis, and treatment timeline), updated receipts, police reports for theft claims, or airline confirmation of cancellation. The appeal needs evidence the original claim didn't include.

- Write a formal appeal letter Address each point in the denial. Quote the specific policy sections that support your claim. Keep it factual. Seven Corners recommends highlighting sections of your policy that directly refute the insurer's stated reason for denying.

- Send it certified mail Send your appeal by certified mail with a return receipt requested. This creates a paper trail proving the insurer received your documents, which matters if you later escalate to a regulator. Most insurers give you 30-90 days to file an appeal, so don't wait.

- Escalate to your state insurance commissioner If the appeal fails, file a complaint with your state department of insurance. The NAIC provides a directory of every state insurance department, and commissioners have the authority to investigate and pressure insurers to re-review claims.

Appeals work more often than people expect. When you can point to a specific policy clause that supports your claim and back it with documentation the insurer didn't have during the initial review, you're giving them a reason to reverse the decision. Insurers prefer settling over regulatory complaints.

Is Travel Insurance Worth It in 2026?

The numbers make a strong case. A U.S. News survey found that 65% of consumers now consider travel insurance important for trip planning, up significantly from pre-pandemic levels. The US travel insurance market hit $7.71 billion in 2025, and roughly half of American travelers now purchase coverage.

Squaremouth's 2024 data shows that claims rose 18% year-over-year, and average payouts jumped 37% to $2,609 per claim. Emergency medical claims became the most frequently filed category for the first time in over a decade, and overtook trip cancellation. That shift reflects both rising medical costs abroad and the growing number of travelers heading to destinations where healthcare isn't free or accessible.

Here's the math. A standard policy costs roughly 6-7% of your trip cost. For a $5,000 trip (roughly €4,600), that's $300-$350 (€275-€320). If anything goes wrong, your coverage limit is typically $5,000-$10,000 for cancellation and $50,000-$100,000+ for medical emergencies. You're paying $300 to protect against a $5,000-$100,000 loss.

When is it NOT worth it? Short domestic trips with fully refundable bookings. Weekend getaways where your total non-refundable spend is under $500. Trips where you already have strong health insurance that covers international care (rare, but some premium plans do). For everything else, especially international trips, trips with non-refundable components over $1,000, and travel during the current period of geopolitical instability, the insurance is worth the cost.

For European travelers, the calculation is slightly different. Your EHIC or GHIC card covers emergency medical treatment within the EU and EEA at local public healthcare rates, but it won't pay for medical evacuation, trip cancellation, or repatriation. If you're traveling outside Europe, or your trip includes non-refundable bookings worth more than a few hundred euros, a separate policy still makes sense. EU residents also have stronger refund rights under the Package Travel Directive for package holidays, which can reduce the need for cancellation coverage.

Tools like TripProf help you track all your trip expenses and documents in one place, which makes the insurance decision clearer: when you can see your total non-refundable spend at a glance, you know exactly how much you're risking without coverage.

Your Pre-Purchase Checklist

Before you buy a policy, run through this list. It takes five minutes and prevents the most common reasons for denied claims.

We learned the hard way that "save all receipts" means everything, not just the big ones. The taxi to the hospital, the pharmacy bag, the hotel extension. When you're dealing with a claim six weeks later, you won't remember what you spent unless it's documented.

- Buy within 14-21 days of your first trip deposit (qualifies you for CFAR and pre-existing condition waivers)

- Insure 100% of your prepaid, non-refundable costs

- Check the look-back period for pre-existing conditions (60 vs. 90 vs. 180 days)

- Read the exclusion list for activities you're planning (snorkeling, skiing, mopeds, hiking)

- Verify the policy covers your destination (check war and political instability exclusions)

- Confirm medical coverage is at least $100,000 and evacuation is at least $250,000 for international trips

- Save all receipts, confirmations, and medical records from the moment you book

- EU residents: verify your EHIC/GHIC is current and understand its limits (no evacuation, no trip cancellation, no repatriation)

- Check if your trip qualifies as a "package" under the EU Package Travel Directive for additional refund protections

If you're organizing a trip with friends, keeping everyone's travel documents organized from the start makes the insurance claim process dramatically easier if something goes wrong. And if you're splitting trip costs with a group, make sure each person has their own policy, because group policies are rare and individual coverage gives everyone independent claim rights.

Frequently Asked Questions

Does travel insurance cover flight cancellations due to war?

No. Standard travel insurance excludes losses caused by war, acts of war, military operations, and government-ordered airspace closures. Only Cancel For Any Reason (CFAR) policies cover war-related cancellations, which reimburse 50-75% of non-refundable costs.

How much does travel insurance cost on a $5,000 trip?

A standard policy typically costs 4-10% of your trip cost, so $200-$500 for a $5,000 trip. The average across all policies in 2024 was roughly 6-7% of insured trip expenses, per NerdWallet.

What's the difference between trip cancellation and Cancel For Any Reason?

Trip cancellation covers a specific list of named reasons (illness, death, natural disaster, terrorism). CFAR covers literally any reason, including fear of travel or simply changing your mind, but reimburses only 50-75% instead of 100%.

Can I buy travel insurance after booking if I have a pre-existing condition?

Yes, but you must buy within 14-21 days of your first trip deposit to qualify for a pre-existing condition waiver. After that window, any condition that was unstable during the look-back period (60-180 days) will be excluded.

Does travel insurance cover medical evacuation?

Yes. Most standard policies include medical evacuation coverage. Experts recommend at least $250,000 in evacuation coverage for international travel, because a single air ambulance transport can cost $25,000-$250,000 depending on location.

What should I do if my travel insurance claim is denied?

Read the denial letter, gather new documentation that addresses the specific reason for denial, write a formal appeal citing your policy terms, send it by certified mail, and escalate to your state insurance commissioner if the appeal fails.

Does travel insurance cover adventure activities like skiing or scuba diving?

Usually not in base policies. Most standard plans exclude activities classified as "hazardous" or "adventure sports." You'll need an adventure sports rider or add-on, which typically costs $20-$100 extra, to cover skiing, scuba diving, hiking above certain altitudes, and similar activities.

Key Takeaways

- Standard travel insurance covers trip cancellation for named reasons, emergency medical care, evacuation, and baggage delays, but excludes war, pre-existing conditions, and adventure sports by default.

- Buy your policy within 14-21 days of your first trip deposit to qualify for pre-existing condition waivers and CFAR eligibility.

- The February 2026 Middle East conflict exposed how war exclusions leave travelers unprotected, even in countries not directly involved in combat.

- Cancel For Any Reason (CFAR) costs 40-50% more but is the only policy type that covers geopolitical disruptions, fear of travel, and last-minute changes of plan.

- One-third of claims get denied, and documentation problems are the top cause. Save every receipt, confirmation email, and medical record from the day you book.

- Fight denied claims by gathering new documentation, filing a formal appeal citing specific policy clauses, and escalating to your state insurance commissioner if needed.

- For international trips, ensure at least $100,000 in medical coverage and $250,000 in evacuation coverage. Track all your trip costs and documents in one place so you know exactly what's at stake.

- Before buying, check the look-back period, read the activity exclusion list, and verify your destination isn't subject to a war or political instability exclusion.

Sources

- News4Jax / Squaremouth: Why 33% of travelers are being denied travel insurance claims (September 2024)

- Squaremouth: Travel insurance payouts rose 37% to $2,609 average in 2024

- NerdWallet: Average travel insurance costs 6-7% of trip expenses

- CNBC: Iran strikes disrupt flights, travel insurance may fall short (March 2026)

- Allianz Travel Insurance: Coverage alert for war in the Middle East (February 2026)

- CDC Yellow Book: Travel insurance, health insurance, and medical evacuation recommendations

- Allianz Partners: Emergency medical transportation costs ($25,000-$250,000+)

- U.S. News: Best Cancel For Any Reason travel insurance companies (2026)

- US Department of Transportation: Automatic refund rule for airline passengers

- Squaremouth: Pre-existing condition look-back periods (60-180 days)

- U.S. News: 65% of consumers consider travel insurance important (2025 survey)

- NAIC: How to file a complaint against insurance carriers

- Emergency Assistance Plus: 35+ travel insurance statistics for 2026

- InsureMyTrip: Pre-existing condition waiver requirements

- Squaremouth: Sports and activities travel insurance coverage

- U.S. News: Best adventure travel insurance companies (2026)

- NerdWallet: How Cancel For Any Reason insurance works

- Seven Corners: How to properly appeal a denied travel insurance claim

- Insurance Journal: Travelers stranded by war learn insurance won't cover cancellations

- CNBC: Airlines cancel hundreds of flights after US, Israeli attacks on Iran

Last updated: July 3, 2026

Keep Reading

More travel tips and guides picked for you

Phone Stolen Abroad? What to Do First, Step by Step

The warm spot where your phone used to be. A stolen phone abroad is a race to protect your money and identity. Here's the exact order to lock it down, suspend your number, get back in, plus the setup that prevents the next one.

How Much Time You Need Between Connecting Flights

The safe gap between connecting flights comes down to one question: how many booking references do you have? One ticket means the airline protects you. Separate tickets mean you are on your own. Here is how to size the buffer and avoid getting stranded.

World Cup 2026 Heat Survival Guide: What Fans Can Actually Bring

FIFA changed the water bottle rule twice in the week before kickoff. Here's what's actually true as of June 10: the sealed-bottle rule, the clear bag policy, which stadiums have AC, and why your real heat risk is the 2-4 hours outside the gates.